Expensing Stock Options

This topic provides overviews of expense option types, estimating forfeitures, and repricing awards and discusses how to run the FAS 123 Option Expense report.

|

Page Name |

Definition Name |

Usage |

|---|---|---|

|

ST_RUNCTL_STFS007 |

Run the FAS 123 Option Expense report (STFS007) to calculate option expenses. |

In compliance with FAS 123R, PeopleSoft Stock Administration allows you to use four combinations of accounting distribution and valuation methods to expense options:

Single valuation method with ratable distribution.

Single valuation method with straight-line distribution.

Multiple valuation method with ratable distribution.

Multiple valuation method with straight-line distribution.

Note: PeopleSoft Stock Administration does not support the accelerated attribution method for expensing options.

Under FAS 123R, stock option grant expenses must initially be calculated using a forfeiture estimation and the expense recorded must later be reconciled based on actual forfeiture outcomes. When a grant vests, the total of expenses taken over time must be equal to the grant's value. Similarly, if an employee terminates or otherwise forfeits an unvested grant, the total of expenses taken over time must be equal to zero. In every expense period, the expense to date for some grants will be based on a forfeiture estimate, while the expense-to-date for others will not because they reflect vesting and forfeiture events in the period.

The Estimated Annual Forfeiture Rate is used to estimate the annual percentage of currently unvested, granted shares that are expected to be forfeited prior to vesting. The rate can be changed from period to period based on experience and events in order to maintain estimation accuracy. The system assumes that the full estimated forfeiture percentage applies at the beginning of the life of a grant and then decreases towards zero as the grant's vest date approaches in order to accurately calculate the estimated rate.

Under FAS 123R, expenses for repriced shares are calculated using a fixed amount of additional expense.

The incremental cost for repriced awards is the excess, if any, of the fair value of the modified (new) award over the fair value of the original (cancelled) award immediately before its terms are modified. When re-valuing the original award at the cancellation date, the term is based on the remaining original term.

Example

To illustrate how repricing expenses are calculated under FAS 123R for both the original and replacement options, use the example of Worldwide Enterprises Corporation, which grants options having a fair market value of $1,500,000 on January 1, 2007. The options are scheduled to 100% vest on December 31, 2009. Worldwide Enterprises' stock price subsequently declines and by December 31, 2007, the options are underwater. On that date, Worldwide Enterprises reprices the options by canceling them and granting replacement options priced at the current market value of the stock.

The repricing expense for Worldwide Enterprises under FAS 123R are determined as of the date the replacement options are granted and, except for forfeitures, are not adjusted further. Since the repricing occurs one-third of the way through the service period, assume that the company has already recorded $500,000 in expenses to date for the underwater options. Worldwide Enterprises must continue to record the remaining $1,000,000 expense for the underwater options. In addition, the company must determine the incremental expense for the replacement options.

The incremental expense is the difference between the fair market value of the replacement options and the underwater options at the time they are cancelled. In this example, assume that the fair market value of the replacement options is $600,000, and that of the cancelled underwater options is $200,000. The incremental expense is $400,000 ($600,000 - $200,000). Worldwide Enterprises records a total expense of $1,900,000 (the original option expense of $1,500,000 plus the $400,000 incremental expense for the replacement options). Since the company has already recorded $500,000 of the original expense before the repricing, it records an expense of $1,400,000 over the service period of the replacement options.

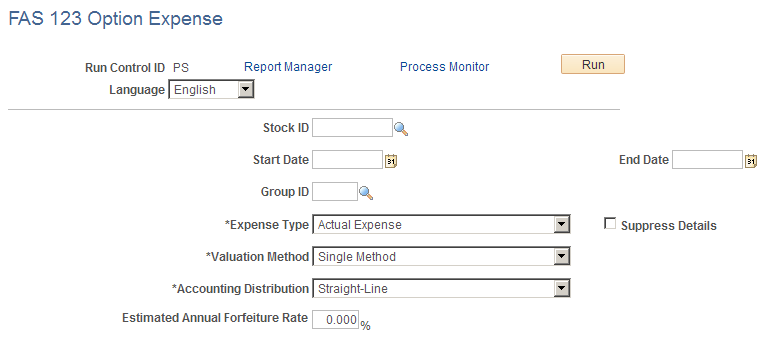

Use the FAS 123 Option Expense page (ST_RUNCTL_STFS007) to run the FAS 123 Option Expense report (STFS007) to calculate option expenses.

Navigation:

This example illustrates the FAS 123 Option Expense page.

Field or Control |

Description |

|---|---|

Start Date and End Date |

Enter the beginning date and ending date for the expense period for which the report is to be run. The date will determine which grants are included in the report. The system does not include in the report grants that are fully vested before the start date or grants with a grant date later than the end date. Important! Run separate reports for the period that you use APB 25 as your accounting standard and the period that you use FAS 123 as your accounting standard. Running the report for dates that straddle the two accounting standards does not produce appropriate results. |

Expense Type |

Select the expense type: Actual Expense, Actual Expense/Proforma Expense, or Proforma Expense. |

Suppress Details |

Select this check box to limit the fields displayed in the report. |

Valuation Method |

Select the method used to calculate the value of shares within a grant:

|

Accounting Distribution |

Select the distribution method used to calculate attribution expenses:

|

Estimated Annual Forfeiture Rate |

The estimated percentage of shares per year that will likely not vest over the life of the grant. |